The Tax Exemption Everyone Is Talking About Doesn't Cover Consulting — We Wish It Did

The Tax Exemption Everyone Is Talking About Doesn't Cover Consulting — We Wish It Did

The same question reached us three times in a single week, from three people who don't know each other: "We've heard Türkiye now fully exempts services provided to clients abroad. We offer consulting to clients in the Gulf — does the decision cover us?"

The short answer: exporting advice is not, by itself, enough.

The precise answer is that the decision granted a substantial tax deduction to a specific list of services — it did not grant it to everyone who issues an invoice to a client outside Türkiye.

We write this as an affected party, not a bystander. Consulting is our profession; whatever applies to you applies to us. And perhaps that is exactly why we can explain the decision as it is: no alarm, no varnish.

Where did the buzz come from?

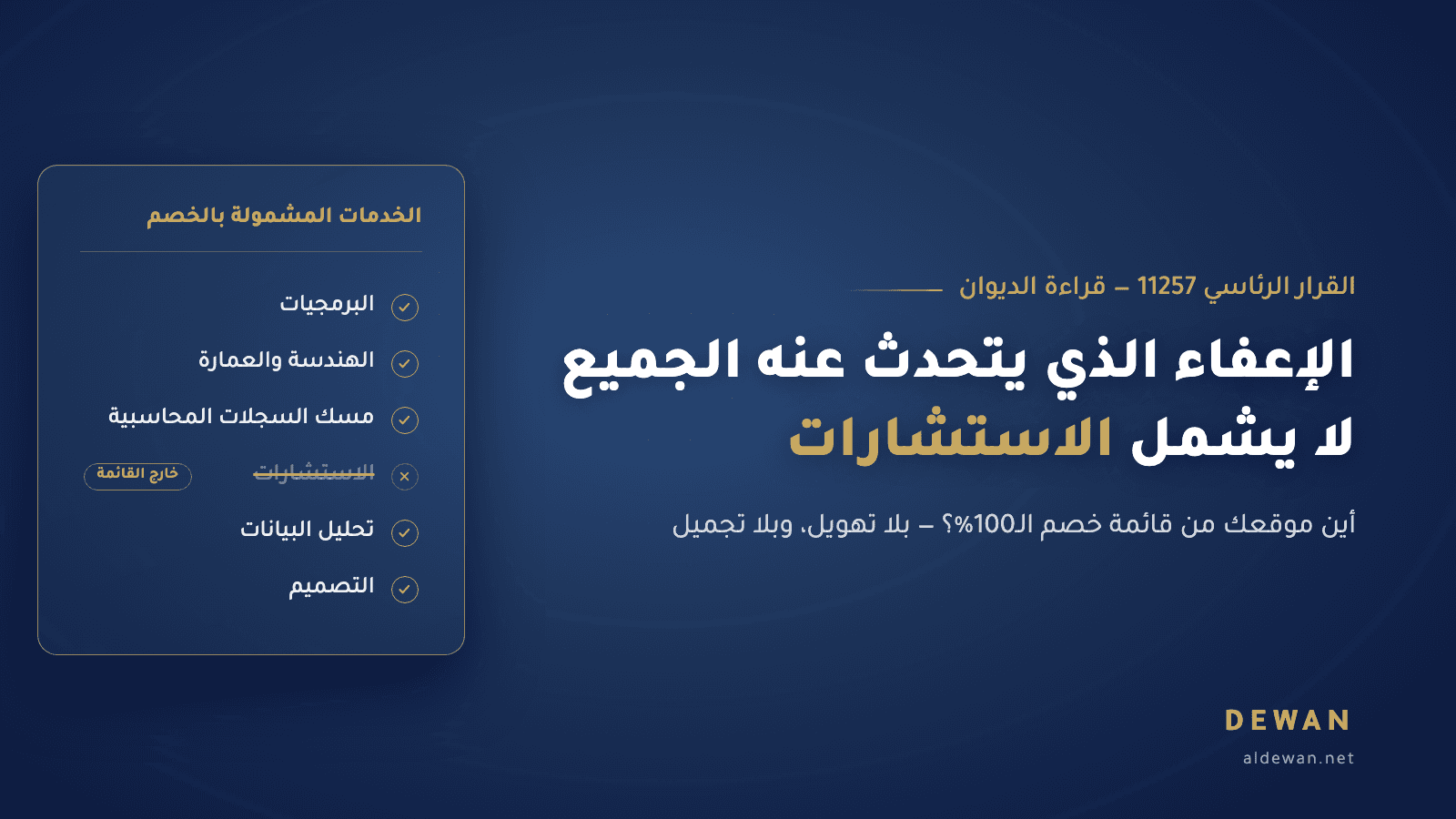

On 30 April 2026, Presidential Decree No. 11257 was published in the Official Gazette, issue 33239. It raised the deduction rate applied to profits from certain services provided from Türkiye to clients abroad from 80% to 100%.

And so the headlines appeared: "Türkiye scraps taxes for service exporters."

An understandable headline — but not the whole story.

The decree did not open the door to all services. It changed the deduction rate for a specific list set out in Article 10/1-ğ of Corporate Tax Law No. 5520 and Article 89/13 of Income Tax Law No. 193.

The list covers:

- Architecture, engineering, design and software.

- Medical reporting and bookkeeping.

- Call centers, product testing and certification.

- Data storage, data processing and data analysis.

- Certain vocational training services.

- Education and health services subject to special conditions and permits.

General consulting is not on that list.

Consulting sits outside the deduction — and the wording is clear

This is not a legal gap waiting for a generous interpretation.

The official communiqués and interpretations of this deduction state that a qualifying service must actually be performed in one of the listed fields. Assistance, consulting and intermediation services connected to those fields do not fall within the deduction merely because they relate to them.

An engineer who prepares a complete engineering design for a project outside Türkiye may fall within the deduction. Someone who provides a separate advisory review, limited to opinions and recommendations, does not qualify automatically.

A software company that develops a system and delivers it to a client abroad may qualify. Someone who assesses the client's needs, recommends suitable systems and supervises an external vendor without actually developing the software is closer to consulting.

The same distinction shows up in accounting: bookkeeping is on the list; tax advisory is not on it merely because its subject matter is accounting.

We know how this lands, because we are the first to feel it. Dewan's profits from consulting services to clients outside Türkiye do not qualify for the deduction merely because the client is foreign.

We will not dress up for you what was not dressed up for us.

The name you use does not decide your tax treatment

Here begins the territory that deserves real attention.

Many who call themselves "consultants" sell more than advice. And some companies registered under technical activities do little more, in practice, than give opinions and supervise.

So ask yourself: what does the client actually receive from you?

An opinion, a recommendation and an action plan?

Or a finished product or deliverable: a program, a blueprint, a design, a processed database, an analytics dashboard, or properly kept books?

The answer helps clarify the nature of the service, but it is not the only thing that decides your position. The inspector doesn't just read the name on your website, and doesn't stop at the activity code in the tax registry.

He looks at the full picture:

- The company's objects as stated in its articles of association.

- The nature of the signed contracts.

- How the service is described on the invoices.

- The actual work and deliverables.

- How revenues and expenses are recorded.

- Who benefited from the service, and where.

If your paperwork says "consulting" while your real work is software development, you may lose a deduction whose eligibility could have been examined.

If you write "software development" while your real work is consulting, the problem is worse: you are building a tax position not on the reality of the activity, but on a label that won't survive an audit.

The Turkish tax system is built on disclosure. The correct description is not a form you fill in when the company is founded and then forget; it is a tax decision that must match what you actually do, every year.

What if your work combines execution and consulting?

That is the situation of many real firms.

You might open a project by analyzing the client's needs, then advise, then deliver a program, a design or another qualifying service. Part of the fee may relate to execution, another part to supervision and recommendations.

The presence of consulting does not necessarily cost you the deduction on the whole project. But benefiting correctly requires separating the activities — and the revenues and expenses attached to each.

Applying the deduction can be examined for the profit generated by the qualifying activity, while the profit from consulting stays in the ordinary tax base.

That separation needs clear contracts, invoices that describe each service precisely, and accounting records that allow each activity's revenues and costs to be identified.

If everything is placed in one contract and one invoice under a general heading like "consulting and technical services," proving the qualifying part may become harder than it ever needed to be.

Clean books don't just fix the past. Sometimes they protect a tax right that a vague wording would have cost you.

100% does not always mean the company pays zero

This point was missing from many headlines.

The decree raised the deduction from the tax base to 100%. That gives a qualifying activity a major advantage — but it does not mean every qualifying company's final tax will necessarily reach zero.

Companies may also be subject to the domestic minimum corporate tax introduced by Law No. 7524 (Official Gazette, 02/08/2024), which began to apply at 10% under its own rules and calculations. The effect of the deduction and the minimum tax must therefore be computed together before telling any company its profits are now fully exempt.

And being on the list is not enough by itself. Core conditions for benefiting include:

- The service must be provided from Türkiye to a non-resident person or entity.

- The benefit of the service must arise exclusively outside Türkiye.

- The entire profit connected to the qualifying activity must be transferred to Türkiye by the deadline for filing the annual return that covers it.

- The records must make it possible to prove the amount of profit generated by the qualifying activity.

This is why we prefer to call it a 100% deduction, not a blanket promise of zero tax.

The difference between the two phrases is not linguistic. It can be the difference between a correct tax projection and a surprise at filing time.

So what does a non-qualifying consultant pay?

If the activity runs through a limited or joint-stock company, the base corporate tax rate is 25% of taxable net profit.

When profits are distributed to shareholders, a 15% withholding applies under Presidential Decree No. 9286 (Official Gazette, 22/12/2024). Profits kept inside the company, or added to capital through the legal procedures, are not treated as a cash distribution.

Nor does the 15% withholding always end the story. A resident individual shareholder may face an additional assessment in his income tax return, depending on the amounts distributed and his tax position, with the applicable exemptions applied and the withheld tax credited under the rules in force.

If you work as an individual in an independent activity, your net profit is taxed on the progressive income tax brackets, which start at 15% and reach 40%.

There is no separate profit distribution here; the activity's profit belongs directly to its owner.

Heavy? Yes — especially next to an activity that qualifies for the deduction.

But profit tax is not the only tax that matters to someone serving clients abroad.

The exemption that actually covers consulting: VAT

The deduction above concerns profit tax. Value added tax (KDV) follows different rules.

Article 11/1-a of VAT Law No. 3065 exempts exported services, while Article 12/2 sets two core conditions:

- The service is provided to a client outside Türkiye.

- The service is used and benefited from outside Türkiye.

This exemption does not rely on the same closed list — which is why it can cover consulting services.

If you advise a company in Riyadh on its business and markets outside Türkiye, and the invoice is issued to the foreign entity, the service can fall within the VAT exemption for exported services.

But a foreign client is not enough on its own.

If the advice concerns the client's branch in Türkiye, or goods it will import into the Turkish market, or an activity that will be carried out and benefited from inside Türkiye, the benefit may be deemed to have occurred in Türkiye — and the service becomes subject to VAT.

The difference is not the client's nationality. It is where the service is actually used.

You may deal with two companies carrying the same trade name: a head office abroad and a branch in Türkiye. The first receives an invoice without VAT for a service tied to its business abroad; the second receives an invoice with VAT for a service used inside Türkiye.

Two clients with similar names — two entirely different tax treatments.

The word "consulting" in your company name does not, by itself, disqualify you — and the word "software" does not, by itself, qualify you.

What decides your position is the work you actually perform, what you deliver to the client, how your contracts, invoices and books describe it, and where it is used.

So don't start from the question: what should we call the activity so it fits the deduction?

Start from a harder, more honest question: what do we actually sell?

Because the tax system doesn't read the sign on your door. It reads the story your documents tell — and trouble begins when the documents don't all tell the same story.